How the War with Iran Is Pushing North Atlanta Mortgage Rates Higher (And What to Do About It)

By Alison Belknap / Compass Real Estate

Almost every buyer I am working with right now is asking some version of the same question. What is happening with mortgage rates, and is it worth doing anything until they come down? It is a fair question. Rates dipped below six percent for the first time in years back in February, and then almost overnight they climbed back up. If you are confused about why, you are not alone.

Here is the short version, and then what it actually means for buying or refinancing a home in North Atlanta this spring.

Why are mortgage rates rising in May 2026?

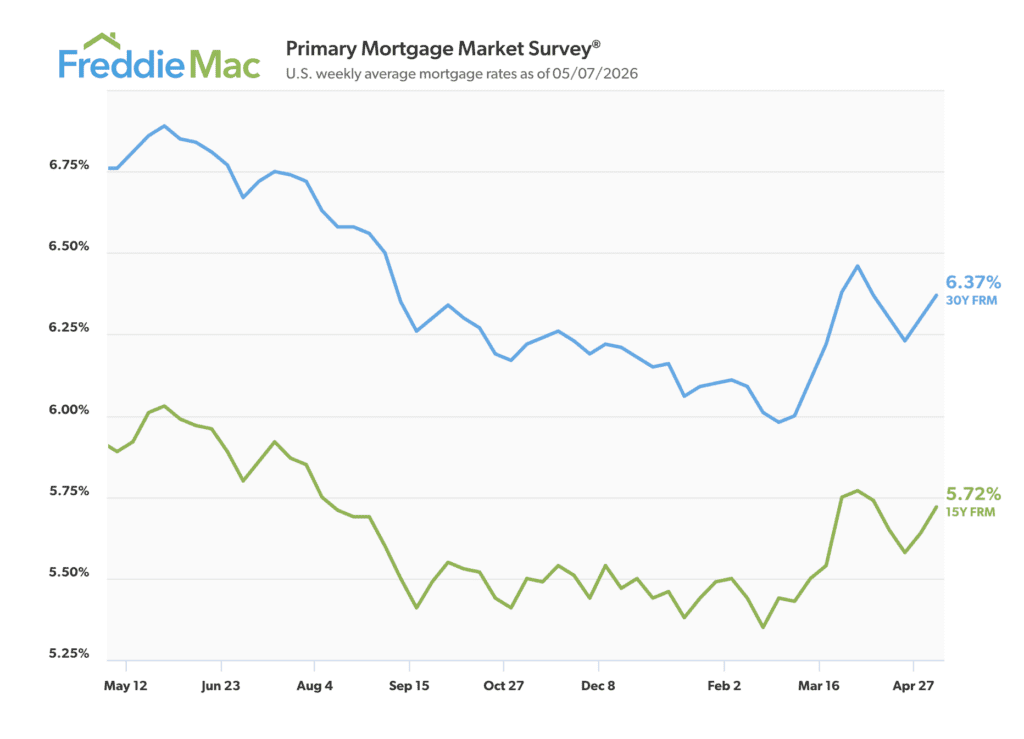

After almost dropping to five percent for qualified buyers in mid-February, the average 30-year mortgage rate climbed back above 6.3 percent by late March. According to CBS News, the trigger was the start of the U.S. war with Iran, which fed inflation fears and pushed yields on the bonds that mortgage rates track higher.

As of May 8, 2026, Zillow data places the 30-year fixed rate at 6.37 percent and the 15-year at 5.75 percent. Refinance rates are running slightly higher, with the 30-year refi around 6.43 percent. These are averages, so your actual offer will depend on your credit profile, down payment, loan type, and the lender you shop with.

The Federal Reserve has held its benchmark rate steady three times this year and has no May meeting on the calendar, so any near-term relief is more likely to come from market dynamics than from the Fed itself.

What does the war with Iran have to do with my mortgage?

The connection is less direct than people assume, but it is real. Mortgage rates do not move in lockstep with the Fed. They move with the bond market, particularly the 10-year Treasury yield. When investors expect more inflation ahead, they demand higher returns on those bonds, and mortgage rates follow.

The war has pushed oil prices up, and oil prices feed into the cost of almost everything that gets manufactured, transported, or shipped. The March consumer price index, the latest available reading, came in at 3.3 percent year over year, the fastest pace since April 2024 according to U.S. News reporting on Bureau of Labor Statistics data. That is the kind of number that keeps bond investors cautious and keeps mortgage rates from drifting back down.

The next inflation reading is due from the BLS later this month and will probably move rates in one direction or the other. So if you are watching the news cycle, that is the date to watch, not the next Fed meeting.

Should I wait to buy a home in North Atlanta?

This is the question I get most, and my honest answer is that it depends less on rates than people think.

Here is what is actually happening in our market. Inventory across metro Atlanta was up 15.5 percent year over year in March, according to Homes.com data, putting Atlanta third in the country for total active listings. The median sale price held near $395,000, basically flat year over year. Days on market are longer than they were during the 2021 to 2023 frenzy. Translation: there is more to choose from, sellers are more open to negotiation, and the buyer who shows up prepared has more leverage than they have had in years.

If you wait for rates to fall, here is the math you have to weigh. When rates drop noticeably, a lot of buyers who have been sidelined come back at once. That demand surge tends to push prices up. So you might save on the rate and lose on the purchase price. Or worse, find yourself in bidding wars again. The old line about dating the rate and marrying the house exists because there is truth to it. You can refinance later. You usually cannot un-overpay.

That said, if your job, life timeline, or financial picture means waiting a year is fine, waiting a year is fine. The wrong reason to buy is fear of missing out. The right reason is that the home and the timing fit your life.

Should I refinance my North Atlanta home now?

If you bought between mid-2023 and late 2024, there is a real chance the math works in your favor right now, especially if your current rate is 7 percent or higher. The traditional rule of thumb is that you need at least one full percentage point of savings to make refinancing worthwhile, but with smaller closing costs and shorter break-even windows on some loan products, even half a point can pencil out depending on how long you plan to stay in the home.

A few things worth doing this month if you are considering it. Pull your current rate and your remaining loan balance. Get one or two refi quotes so you have actual numbers, not estimates. Run the break-even math, which is closing costs divided by monthly savings, and see how that compares to how long you plan to stay. If the answer is shorter than your timeline, it is worth a closer look. If rates do drift down later this summer, having your paperwork ready means you are not scrambling.

What does this mean for North Atlanta sellers?

Inventory is up, but North Atlanta is not a uniformly soft market. The patterns I have written about before still hold. Renovated homes in top school districts, including Walton, Pope, Lassiter, and Wheeler in East Cobb plus the strong Roswell, Alpharetta, and Johns Creek districts, are still moving quickly when priced correctly. The homes sitting on the market are usually overpriced for their condition or in less competitive locations.

If you are thinking about selling this summer, the right move is not to chase last year’s price expectations. It is to get accurate data on recent comparables in your specific neighborhood, fix the things buyers will flag at inspection, and price competitively from day one. Homes that need three price reductions to find a buyer almost always net less than homes priced right out of the gate.

My honest read for the next 60 days

The experts CBS News spoke with are forecasting May rates to stay roughly between 6.2 and 6.4 percent, with a slight downward bias if inflation cooperates. That is not a dramatic move in either direction.

If you are buying, focus on what you can control. Your credit profile, the lender you choose, the home you buy, and the price you negotiate. If you are refinancing, get your numbers ready now so you can move quickly if rates dip.

And if you want to talk through what any of this means for your specific situation in East Cobb, Roswell, Alpharetta, or Johns Creek, that is exactly what I do. Call or text 617-605-5939 or set up a no-pressure 30-minute consult below.

May 8, 2026

Be the first to comment